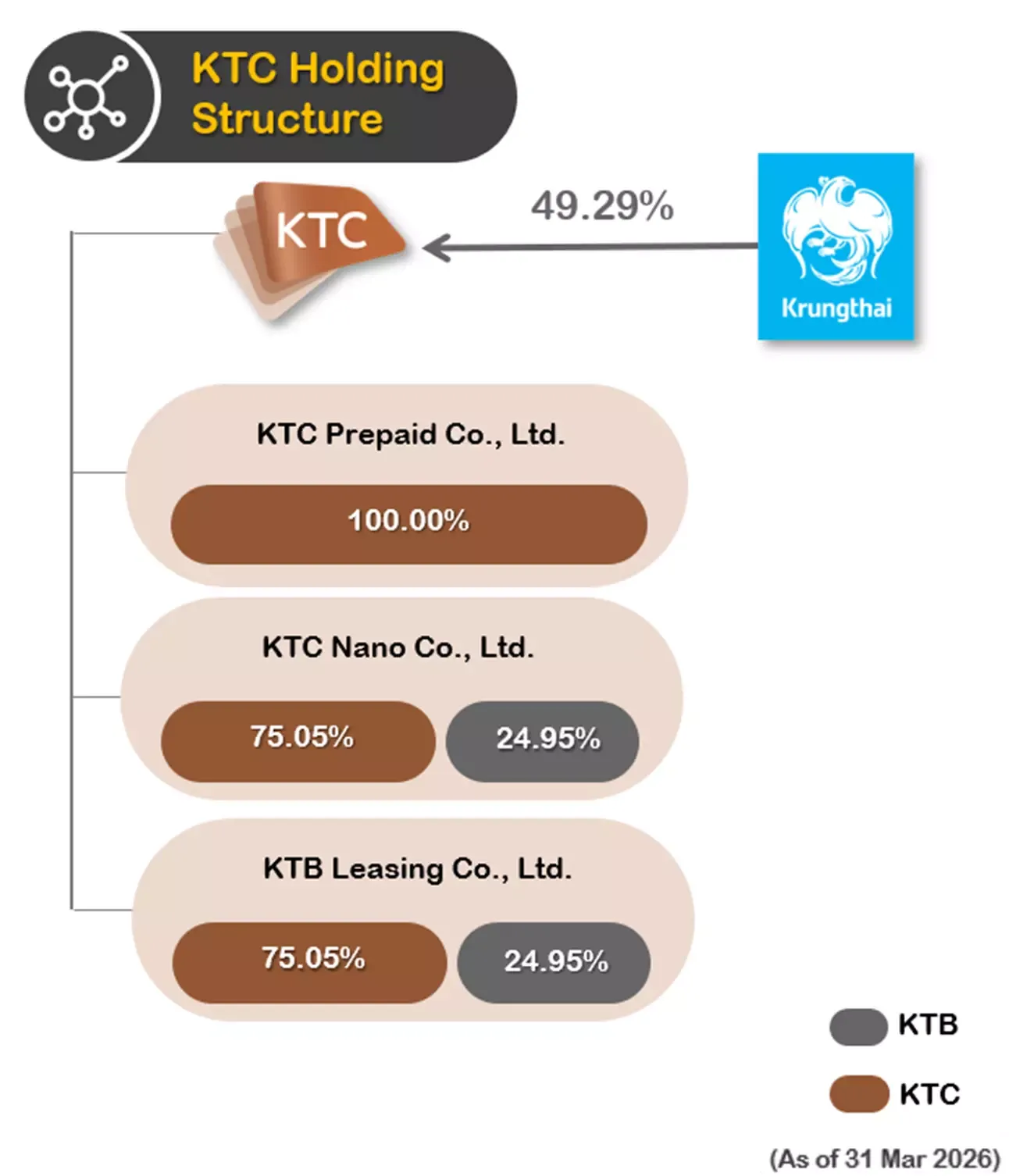

1.

* Remark: As of January 9, 2026, KTC Prepaid Company Limited received approval from the Bank of Thailand to return its business licenses. Consequently, Krungthai Card Public Company Limited has officially notified the Stock Exchange of Thailand regarding the dissolution of the subsidiary's status.

2.

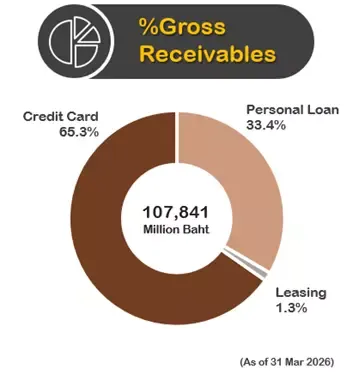

KTC operates in retail consumer finance business including unsecured loan which are credit card and personal loan business. As of 1Q2026, Total receivables are stated below.

3.

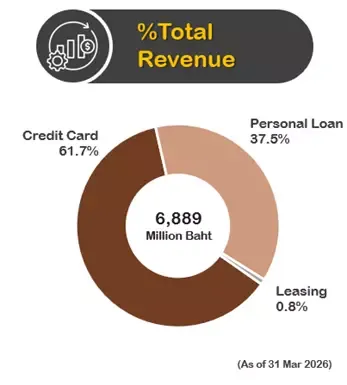

The revenue structure of KTC consisted of interest income and fee income from two main businesses: credit card business and personal loan business, including leasing business. details shown in the chart below.

4.

5.

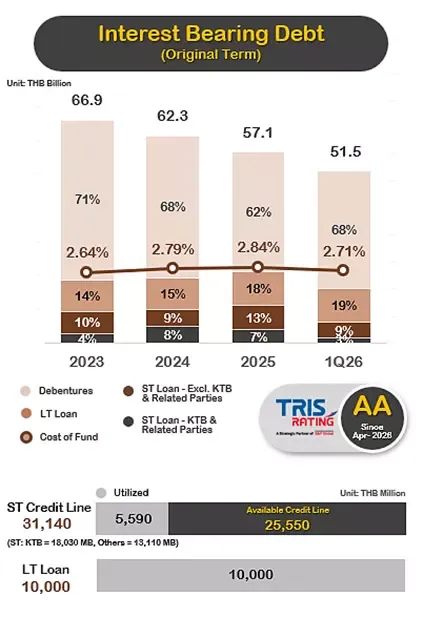

As of 1Q2026, the Group maintained a stable capital structure with diversified funding sources. Total borrowings (including lease liabilities) amounted to THB 51,518 million, comprising 56% long-term borrowings and 44% short-term borrowings (including the portion of loans and debentures due within one year). KTC utilizes comprehensive funding channels, including Thai commercial banks, securities companies, insurance companies, and various funds. This consists of short-term borrowings from Krungthai Bank and related parties totaling THB 1,690 million, short-term borrowings from other financial institutions of THB 4,530 million, long-term borrowings from Krungthai Bank of THB 10,000 million, and debentures of THB 35,130 million. Debentures account for approximately 68% of total borrowings, underscoring strong investor confidence and the Company's effective access to debt capital markets.

Apart from capital structure management, the Group remains committed to disciplined financial oversight. The D/E ratio as of 1Q2026 declined to 1.30 times, significantly lower than the 1.58 times recorded in the same period last year. This decrease was primarily driven by two factors: 1) strong profit accumulation, which strengthened the equity base, and 2) a reduction in borrowings aligned with cautious portfolio expansion amid the economic slowdown, which mitigated the need for additional funding. Furthermore, the current D/E ratio remains well below the debt covenant of 10 times, demonstrating high financial flexibility to expand the business or absorb future economic volatility.

Liquidity: As of 1Q2026, the Group maintained available credit lines totaling THB 25,550 million. Concurrently, debentures and long-term borrowings maturing within the remainder of 2026 amounted to THB 15,330 million. The Company’s liquidity significantly exceeds its upcoming debt obligations, underscoring a robust liquidity position and minimal short-term default risk.

6.

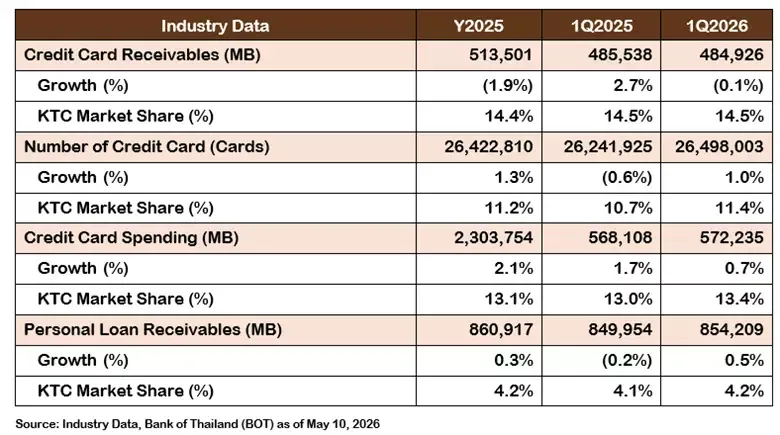

According to Bank of Thailand data at the end of March 2026, industry-wide credit card balances totaled THB 484,926 million, representing a decline of 0.1% (YoY). Meanwhile, industry personal loan balances reached THB 854,209 million, an increase of 0.5% (YoY). For the first quarter of 2026, total industry credit card spending volume amounted to THB 572,235 million, reflecting a marginal expansion of 0.7% (YoY). This industry growth rate was outpaced by KTC’s credit card spending volume, which grew by 3.7% (YoY) or an amount of THB 76,800 million.

Despite a continuous contraction in the overall consumer finance industry due to economic uncertainty and more stringent lending standards among financial institutions, KTC maintained its market share across all core products. During the first quarter of 2026, KTC’s market share in credit card receivables held steady at 14.5% (YoY). Market share for card spending volume grew to 13.4% from 13.1% (YoY), while the personal loan receivables market share increased to 4.2% from 4.1% (YoY).

As of the end of the first quarter of 2026, KTC's total membership reached 3,732,625 accounts, comprising 3,019,095 credit cards, up 8.0% (YoY), and 713,530 personal loan accounts, an increase of 3.4% (YoY).

7.

The company pays good attention on every step of the operation. We are very selective on approval process and performs well on debt collection. In addition, our management always pays close attention to the debt collection process. As a result, the company could perform well on debt collection and has good credit quality. Bad debt recoveries in 1Q26 amounted to THB 979 million, a 1.8% (YoY) decrease. The Company continues to maintain effective debt collection efficiency despite challenging economic conditions.

8.

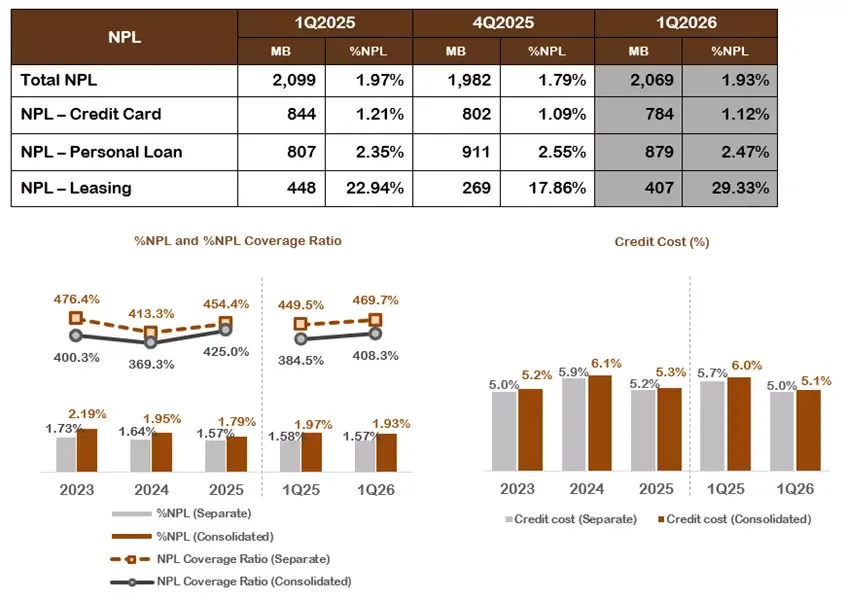

In 1Q2026, the Group’s non-performing loans to total loans ratio (%NPL) stood at 1.93%, a slight decrease from 1.97% in the same period last year. For the separate financial statements, the %NPL remained low at 1.57%, down slightly from 1.58% in 1Q2025, underpinned by continuous asset quality management and the rigorous screening of applicants.

The Group’s NPL Coverage Ratio increased to 408.3% from 384.5%, while the ratio for the separate financial statements rose to 469.7% from 449.5% compared to the first quarter of the previous year, respectively. These high coverage levels reflect a prudent approach to portfolio management and ensure portfolio strength and stability.

The Group’s total Credit Cost for 1Q2026 was 5.1%, down from 6.0%, while that of the separate financial statements was 5.0%, down from 5.7%, compared to the same period in 2025, respectively. This reflects the successful management of overall asset quality in accordance with established targets.

9.

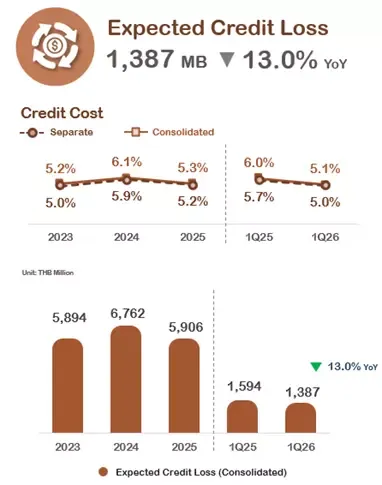

The Group’s Expected Credit Loss (ECL) was 1,387 million baht, a 13.0% decrease (YoY), primarily driven by rigorous and consistent applicant screening. This has resulted in higher quality across the majority of the new loan portfolio, reflecting the effectiveness of the Group's credit risk management.

10.

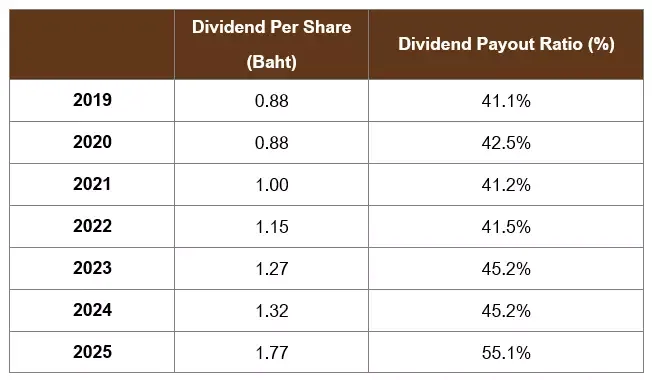

The shareholders’ meeting no. 1/2003 on March 25, 2003, approved the dividend payment policy to pay approximately 40 percent of net profit after deduction of income tax and appropriation for a legal reserve since 2003 onward. The table below shows the dividend payment for the operating result during 2019 – 2025.

11.

KTC has integrated sustainability across economic, social, and environmental dimensions into its business operations, with a commitment to conducting business responsibly, fairly, and transparently. The Company focuses on advancing innovation and digital technology to develop products and services that create value for all stakeholders while effectively reducing environmental and social impacts. This commitment aims to guide both the organization and Thailand toward sustainable growth, reflected through three sustainability pillars: Better Products & Services, Better Quality of Life, and Better Climate, under five strategic frameworks:

Governance Excellence

KTC elevates corporate governance standards to ensure transparency, accountability, and adherence to business ethics. The Company strengthens its risk management and data management systems to support operations and high-quality reporting, thereby building confidence among all stakeholders.

Green Growth

The Company pursues business growth alongside environmental stewardship through initiatives to reduce greenhouse gas emissions, enhance resource efficiency, and promote environmentally responsible behavior across the organization and its supply chain through its products and services. These efforts support national policies aimed at advancing a low-carbon economy and achieving Net Zero greenhouse gas emissions by 2050.

Responsible & Inclusive Finance

KTC develops and delivers financial products and services that enhance the quality of life for all customer segments through fair and equitable access. The Company promotes financial literacy to improve social well-being, while strengthening workforce capabilities as a key driver of the business. In parallel, KTC supports respect for human rights at both the organizational and societal levels.

Digital SD Innovation

The organization is driven by digital technology and innovation to develop value-creating products and services that respond to customer needs. These efforts are accompanied by a strong emphasis on data security and privacy for customers and stakeholders, reinforcing the Company’s sustainable competitive advantage in the digital era.

Culture Transformation

KTC fosters an organizational culture anchored in a 'sustainability mindset,' embedded across all operational processes and employee levels. This is achieved through the integration of sustainability objectives and key performance indicators at both corporate and business unit levels, together with continuous learning and active employee engagement, ensuring that sustainability is truly integrated into KTC’s business practices.

KTC supports the United Nations Sustainable Development Goals (SDGs). Further details can be found at:

https://www.ktc.co.th/sustainability-development

12.

13.

➢ Target & Growth Direction

➢ KTC Direction in 2026

For 2026, KTC will focus on strengthening the existing loan portfolio, sustaining growth in card spending, and increasing investment in digital technology through the rollout of the Company’s new core system. This transformation will enhance operational flexibility, elevate customer experience, and improve overall efficiency. KTC will continue to support the growth of its two core businesses, credit cards and personal loans, while extending into a new business segment, insurance brokerage, to broaden and build sustainable revenue streams. The Company places strong emphasis on comprehensive risk management, leveraging data and advanced analytics to maintain portfolio quality, with a primary focus on preserving asset quality and long-term financial stability.

➢ Sustainable Household Debt Solution Approach and Potential Impacts

KTC consistently implements long-term customer assistance measures in accordance with BOT Notification No. 3/2025 regarding Responsible Lending. These measures aim to strengthen the role of service providers in managing customers throughout the entire debt cycle. KTC approves loans based on individual debt-serviceability to ensure that customers do not face an unreasonable increase in their total debt burden. Key assistance measures include reducing minimum payment rates, converting credit card debt into long-term personal loans, financial burden relief through interest credits, assistance for customers in Severe Persistent Debt (SPD), extending grace periods, and installment reductions.

Furthermore, KTC collaborated with the Bank of Thailand on the 'You Fight, We Help' program to support vulnerable customers in returning to normal repayment status, a program which concluded in September 2025. This includes participation in the 'Debt Cleared, Move Forward' program, involving the transfer of unsecured non-performing loans (NPLs) overdue by more than 90 days. Based on the debt status as of September 30, 2025, eligible customers with total NPLs across all financial providers and loan types not exceeding THB 100,000 per person were transferred to Sukhumvit Asset Management Co., Ltd. (SAM) for debt restructuring and burden reduction. Ownership of these qualifying debts was transferred to SAM effective January 1, 2026.

The Company assesses that the implementation of these programs and assistance measures will not have a significant impact on the Group’s overall performance. Additionally, the Company has already maintained full provisioning for expected credit losses.

Detailed information on customer assistance guidelines can be found at https://www.ktc.co.th/about/news/measure